The purpose of this Client Alert is to provide an update on developments and changes to the Vacant Residential Land Tax (“VRLT”) rules since our client alert on the topic which was issued in February 2024. You can find that earlier client alert here.

The State Taxation Further Amendment Act 2024 received Royal Assent on Tuesday 3 December 2024 which contained additional changes to VRLT. These additional changes are set out below.

Land in alpine resorts excluded from VRLT

The definition of residential land has been modified to exclude land in alpine resorts. VRLT will not be applicable altogether.

Clarification of holiday homes used by a relative of the owner/vested beneficiary

From 1 January 2025, if a relative of the owner or the vested beneficiary uses and occupies the property as a holiday home for at least 4 weeks (whether continuous or aggregate) in a calendar year, and all other requirements are satisfied, the holiday home exemption may apply. For the 2025 tax year, the use of holiday homes by a relative in the 2024 calendar year is included.

A relative of the owner or vested beneficiary includes a spouse or domestic partner, (grand) parents, (grand) children of owner/vested beneficiary or partner; brother, sister, niece or nephew of owner/vested beneficiary and their respective partners.

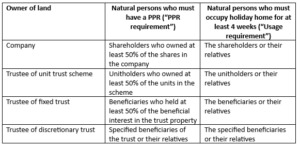

Holiday homes owned by companies and trusts

We mentioned in Client Alert No.100 (which you can access here) that the holiday home exemption did not extend to holiday homes held by companies and trusts at that time, but the Victorian Government was committed to extending the exemption to include companies and trusts in certain circumstances.

The Land Tax Act 2005 has now been amended to provide such exemptions as set out below:

From 1 January 2025, a company or trustee of a trust is eligible for this exemption if:

- They have continuously owned the home since 28 November 2023, when the Government announced this measure. Companies or trustees that entered into a contract to purchase a holiday home on or before 28 November 2023 but settle after that date are also eligible. It is important to note that this exemption does NOT extend to land owned by a company or a trustee of a trust where a contract to purchase a holiday home was entered into after 28 November 2023; and

- There have been no changes in beneficial ownership of the land since 28 November 2023, except for transfers involving relatives; and

- One or more eligible natural persons used another property in Australia as their Principal Place of Residence (PPR) in the preceding tax year and they used and occupied the holiday home for at least 4 weeks (whether continuous or aggregate) in a calendar year as follows:

If a holiday home is owned by a family trust on or before 28 November 2023 (including a purchase contract entered into by that time), it is necessary to review your trust deed to ascertain who are the specified beneficiaries and review whether both the PPR requirement and the usage requirement has been satisfied.

If a holiday home is purchased after 28 November 2023 (contract date) and settled in the 2024 calendar year by a family trust, it will not be liable to VRLT in the 2025 calendar year. This is due to the fact that a change ownership during a calendar year exempts the purchaser from (VRLT) in the following year. However, it is necessary to consider the property’s planned usage in the 2025 calendar year for future VRLT assessment as the company/trust exemption discussed above will not apply.

If a holiday home is purchased after 28 November 2023 (contract date) and settled before 31 December 2023, VRLT is applicable for the 2025 calendar year. Whether VRLT actually applies depends on the usage of the property in the 2024 calendar year. Please contact your Blaze Acumen advisor if this applies to you.

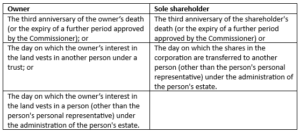

Holiday home exemption extended to deceased estates

From 1 January 2025, the holiday home exemption may continue to apply for a specified period after the owner, or sole shareholder of a corporation that owns the home, passes away. The exemption will continue provided a relative of the owner or the sole shareholder of the landowning corporation:

- uses and occupies other land in Australia as their PPR, and

- uses and occupies the holiday home for a period of at least 4 weeks (whether continuous or aggregate) in the calendar year.

The exemption continues until the earlier of:

Holiday home exemption extended to “contiguous land”

This extension of the VRLT exemption is in the context that from 1 January 2026, VRLT will start to apply to unimproved residential land in metropolitan Melbourne that has remained undeveloped for at least 5 years and is capable of residential development. The exemption applies when:

- The land is unimproved land within the meaning of the Land Tax Act 2005.

- The land is owned by the same owner of the holiday home land.

- The land is contiguous with the holiday home land, or separated from the holiday home land only by a road railway or other similar area across or around which movement is reasonably possible.

- The land enhances the holiday home land.

- The land is used solely for the private benefit and enjoyment of the person who uses and occupies the holiday home land.

The 2026 expansion of VRLT application is only relevant if you have unimproved residential land in metropolitan Melbourne. This exemption is only relevant if your PPR is in regional Victoria and you have a holiday home in Melbourne which you intend to rely on the holiday home exemption.

Other notable topics from SRO Q&A website:

The SRO Q&A website provides useful resource for understanding how VRLT works. You can go to this website here. In addition to the issues discussed above, we have summarised below a number of further items we consider important to know:

- If a person has moved into a retirement home or residential care facility, VRLT does not apply if the home was PPR and can be exempt from land tax under the relevant provisions.

- If a property is vacant for more than 6 months in a calendar year, generally it is subject to VRLT irrespective of whether it is advertised for sale during that time. If a property changes ownership during the year preceding the tax year (e.g. 2024), it is not subject to VRLT for that tax year (e.g. 2025). However, the change of ownership must occur during the calendar year (i.e. settlement takes place no later than 31 December).

- If a property is advertised for rent but you have not been able to secure a tenant to occupy for 6 months in a calendar year, it is subject to VRLT irrespective of whether it is advertised for rent during that time. This is irrespective whether the rental is long term or short term (e.g. via Airbnb). As such, the intention to rent will not allow you to escape a liability to VRLT, only the actual usage. The 6 month rental requirement (i.e to avoid the property being treated as not vacant) can be satisfied by a combination of different rentals, including short terms and long term.

Land owner’s obligation

Owners of land with a vacant residential property are required to notify the State Revenue Office (SRO) by 15 January each year via an online portal. This is the case when the property is considered vacant. If a property is eligible for an exemption (e.g. where you satisfy the holiday home exemption), the land owner is still required to notify the SRO and apply for the exemption via the same portal.

Conclusion

2025 calendar year will be the first year that VRLT becomes relevant to many people due to the expansion of its application to all residential land in Victoria. The reporting due date of 15 January is fast approaching.

Should you require advice in relation to the application of VRLT to your specific circumstances and properties please contact your Blaze Acumen advisor. If necessary, we can also engage with a property lawyer if your requirements extend beyond VRLT Tax advice.

As the responsibility for the income tax and State Revenue taxes applicable to a property rests with the beneficial owner of the property, now is also an opportune time to establish a register of properties held by you, your spouse and your family trusts/companies/superannuation funds. Please contact us if you would like our assistance in establishing such a property register, which should also identify the use of each property and the likely income tax and State Revenue taxes outcome for each property.

Please do not hesitate to contact your Blaze Acumen advisor if you would like to discuss any of the issues raised in this Client Alert.